Introducing ez money: A Digital Lending Player in the United Arab Emirates

The financial technology landscape in the United Arab Emirates continues its rapid evolution, with digital lenders playing an increasingly significant role in providing accessible credit solutions. Among these modern players is ez money, a company positioning itself as a streamlined, app-based provider of short-term unsecured personal loans. Operating within the dynamic UAE market, ez money primarily targets both salaried residents and non-resident visitors, offering what it promotes as swift access to much-needed liquidity.

While ez money aims to cater to a broad segment of the population, particularly expatriates and those seeking emergency funds, a notable characteristic of the company is the limited public availability of its corporate registration and financial details. Information regarding its full legal name, exact headquarters location within the UAE, founding year, and ownership structure remains largely undisclosed in public records. This lack of transparency is a crucial point for any prospective borrower to consider. The business model emphasizes convenience and speed, reflecting a growing trend in digital finance where traditional banking hurdles are bypassed through technological solutions.

ez money’s operational focus is squarely on digital engagement. It eschews physical branches in favor of a mobile application available on both iOS and Android platforms, streamlining the entire loan application and management process. This approach aligns with the UAE's vision for a digitally empowered economy. However, the absence of publicly listed leadership team members or detailed corporate governance information underscores the need for thorough due diligence by anyone considering its financial products. Despite these information gaps, ez money has gained recognition within industry round-ups, suggesting a visible presence in the competitive digital lending space, estimated to serve tens of thousands of users, predominantly individuals aged 25 to 45.

Understanding ez money's Loan Products and Application Process

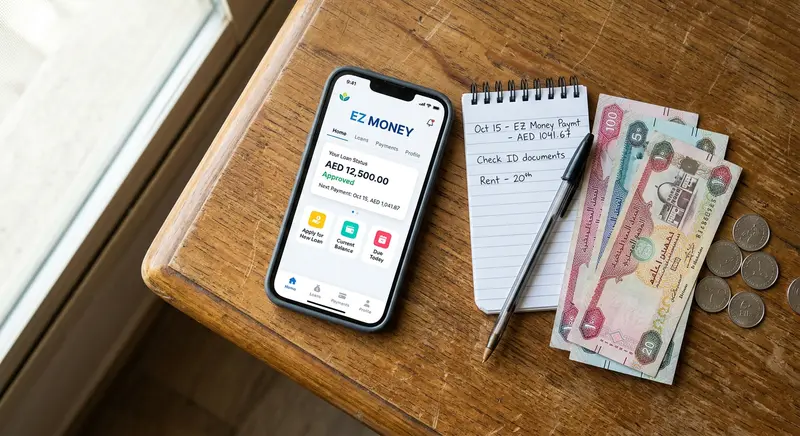

ez money's core offering revolves around personal cash loans designed for immediate financial needs. These are typically short-term, unsecured loans, meaning they do not require collateral such as property or assets. The minimum loan amount specified is AED 10,000, which translates to approximately USD 2,722, making it suitable for significant but not excessively large financial requirements. While a maximum loan amount is not publicly disclosed, industry comparables suggest it likely ranges between AED 30,000 to AED 50,000 for similar digital lenders in the UAE. Beyond direct cash loans, ez money also promotes ancillary services such as prepaid cards and bill-payment functionalities, aiming to provide a more comprehensive financial utility suite.

A critical aspect for potential borrowers is understanding the financial terms. Unfortunately, ez money does not publicly disclose its interest rates or Annual Percentage Rate (APR) ranges. Prospective applicants are required to consult the specific terms and conditions directly within the mobile application before committing to any loan. Repayment periods are generally in line with peer applications, typically spanning 12 to 48 months, though the exact terms for individual loans are not detailed without an application. Repayment is presumed to occur through monthly direct debits from the borrower's bank account, a standard practice in the UAE for salary-based loans. Similarly, information regarding origination fees, processing fees, or late-payment penalties is not publicly available, reinforcing the necessity of scrutinizing all contractual details presented in the app.

The application process for an ez money loan is entirely digital, conducted exclusively through its mobile application. There are no physical branches or website-based applications. The Know Your Customer (KYC) and onboarding procedures involve digital identity verification, typically requiring the upload of an Emirates ID for residents and a selfie. For non-resident visitors, basic document uploads such as a passport and visa are likely required, aligning with general industry norms. ez money is inferred to employ automated, AI-driven credit evaluation for rapid underwriting decisions, a common feature among instant-loan apps in the UAE. Successful applicants can expect loan disbursements via bank transfer to their UAE bank accounts, with potential future integrations for mobile wallet top-ups.

The ez money Mobile Application, Regulatory Claims, and Market Standing

The ez money experience is centered around its mobile application, reportedly available for both Android and iOS devices. This digital platform serves as the sole interface for customers, facilitating quick loan applications, secure document uploads, and providing a dashboard for managing existing loans. While the app's availability is stated, specific app store listings and user ratings are not readily found in public domain research, which can make it challenging for new users to assess its reliability and performance based on community feedback. The design philosophy of such applications typically prioritizes ease of use and speed, reflecting the demands of consumers seeking quick financial solutions.

Regarding its regulatory status, ez money claims to operate under the oversight of the UAE Central Bank. However, a specific license number or public registration details to corroborate this claim are not widely accessible. This lack of verifiable licensing information is a significant point of consideration for any financial service provider in the UAE, where strong regulatory frameworks are in place to protect consumers. While there are no public records of penalties or enforcement actions against ez money, the absence of clear regulatory transparency places a greater onus on borrowers to verify these claims independently. Adherence to standard consumer protection measures, such as clear disclosure of rates and fees within the app, is a requirement under UAE regulations, but the extent of ez money’s compliance can only be fully ascertained upon engaging with their application directly.

In the highly competitive UAE digital lending market, ez money positions itself among a growing number of players. Its competitors include established digital lenders such as Cash Now, FinBin, Flex, IOU, NowMoney, and Credy. A key differentiator for ez money, as per available information, is its reported eligibility for non-residents and tourists, which expands its target market beyond typical resident-focused lenders. While it appears in industry round-ups, direct customer reviews or detailed feedback are not publicly available, making it difficult to gauge overall customer satisfaction or identify common complaints. Customer support is likely provided through in-app channels, as no dedicated helpline or physical customer service centers are reported.

Essential Advice for Prospective ez money Borrowers in the UAE

For any individual considering a loan from ez money, or any digital lender in the United Arab Emirates, exercising due diligence is paramount. Given the limited publicly available information regarding ez money’s specific terms, interest rates, fees, and verifiable regulatory status, potential borrowers must proceed with caution and a thorough understanding of all contractual obligations. The digital nature of the application process, while convenient, means that all critical information will be presented within the app itself, often without a direct human intermediary to clarify complex terms.

Firstly, it is absolutely essential to read and understand every detail of the loan agreement presented within the ez money application before signing. Pay close attention to the Annual Percentage Rate (APR), which encompasses not only the interest rate but also any additional fees. Seek clarity on all charges, including origination fees, processing fees, and especially late-payment penalties, which can significantly increase the total cost of the loan if not managed properly. If these details are not transparently displayed, consider it a red flag. Borrowers should not hesitate to contact in-app support for any clarifications needed.

Secondly, verify ez money’s claim of being licensed by the UAE Central Bank. The Central Bank's website or direct inquiry can often confirm the licensing status of financial institutions operating in the country. Operating with an unregulated lender carries significant risks, including limited recourse in case of disputes or unfair practices. Understanding your rights as a consumer under UAE law is crucial, particularly concerning data privacy and financial disclosures. Always ensure that the lender adheres to consumer protection guidelines.

Finally, always compare ez money’s offerings with those of other reputable digital lenders and traditional banks in the UAE. Different providers will have varying rates, terms, and eligibility criteria. Choosing a loan is a significant financial decision, and selecting the most favorable terms can save a substantial amount over the repayment period. Borrow only what is necessary and ensure that the repayment schedule fits comfortably within your monthly budget to avoid defaulting, which can negatively impact your credit standing in the UAE and potentially lead to legal consequences. Responsible borrowing is key to maintaining financial health.